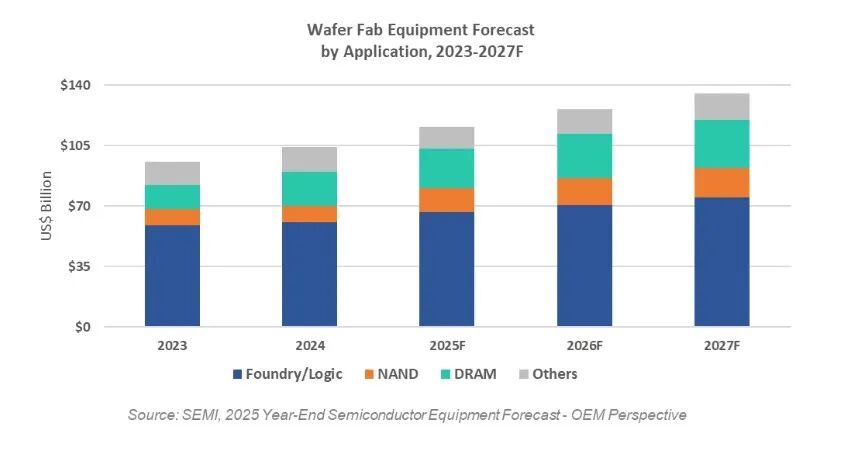

Global semiconductor equipment sales are projected to reach $133 billion in 2025, setting a new record. For equipment suppliers, this milestone is more than a headline—it marks a structural shift in how fabs prioritize investments, upgrade manufacturing capability, and allocate capital. Unlike previous cycles driven by consumer demand, the current expansion is powered by long-term commitments tied to artificial intelligence, advanced memory, and packaging-intensive architectures. This creates a rare combination of scale growth, technology upgrading, and predictable demand for suppliers.

Artificial intelligence workloads do not simply increase wafer volumes. Instead, they amplify the complexity per wafer, which directly increases equipment intensity. Advanced logic nodes require additional lithography steps, tighter process control, and higher utilization of precision etching, deposition, and metrology tools. Even modest wafer expansions translate into disproportionately higher equipment spending. For suppliers, opportunities arise not only from new fab construction but also from process migration, equipment replacement, and yield optimization initiatives.

At the same time, investments in AI accelerators and data center processors are driving strong demand for high-bandwidth and high-performance memory architectures. These upgrades focus on technology advancement rather than raw capacity, creating sustained demand for next-generation manufacturing equipment.

Front-end wafer fabrication equipment remains the foundation of market scale. Investment is increasingly concentrated on advanced logic production lines, memory process upgrades, and selected mature nodes that support AI infrastructure. Meanwhile, back-end equipment is undergoing a structural revaluation. Advanced packaging and testing are no longer auxiliary steps; they are critical to system-level performance and reliability. High-precision bonding, dense interconnect formation, and reliability testing equipment are becoming essential, raising technical specifications, qualification cycles, and supplier stickiness, which benefits capable equipment vendors.

Geographically, equipment spending remains concentrated, but predictability is more important than volatility. Capacity expansions in mature and specialty nodes provide stable demand, while advanced-node investments sustain long-term pull for high-precision tools. Memory-focused regions generate recurring upgrade cycles driven by technology migration. Supported by industrial policy, localized manufacturing, and specialized capacity strategies, these trends reduce the risk of abrupt investment pullbacks and offer equipment suppliers longer planning horizons.

Reaching $133 billion is not just a matter of scale—it reflects a mature market logic. The industry is shifting from cyclical growth to capital intensity driven by process complexity. Suppliers can expect longer customer roadmaps, higher emphasis on process capability over price, and increasing demand for customization, reliability, and service support. Equipment is no longer a one-time purchase but a long-term productivity asset embedded in the customer’s process strategy.

The upcoming growth phase is backed by measurable trends: AI compute requirements, memory architecture evolution, and packaging-driven system integration. For equipment suppliers, 2025 is not merely a strong year; it marks the start of a cycle where technological depth, application alignment, and execution capability define competitive advantage. The real opportunity lies not in timing the cycle but in positioning where process complexity rises most rapidly.